The Government recently announced it would be creating a new Homes Ombudsman that requires all developers to be party to the scheme, giving a route to redress for home buyers should their new property fall short of expectations of feature shoddy work. The National Custom and Self Build Association (NaCSBA) fed into the consultation back in August 2019 to press the case for self builders.

In line with NaCSBA’s submission, the consultation confirmed that the scope of the New Homes Ombudsman will not include self-builders “unless they plan to sell the property to someone else within a set period”.

NaCSBA is supportive of this approach, but confirms that the ‘period’ referred to will need qualifying. Self building with the intent to sell has other consequences, such as the Community Infrastructure Levy (CIL) exemption, and puts self build in to a separate category, making it more akin to speculative building.

The confirmation is helpful, as a self build typically involves large numbers of suppliers of services, skills and resources, and the co-ordination of these elements into a new home, which makes them a poor fit for the Ombudsman scheme.

NaCSBA recommends self builders choose from its members when sourcing contractors and businesses for work, as its own Code of Practice offers a route to dispute resolution should a consumer have issues with a contractor. All NaCSBA members (apart form Not for Profit members, such as councils) must sign up to the scheme as a condition of membership. Equally, self builders should look out for members of other trade associations, such as the Federation of Master Builders or the Structural Timber Association also offers surety that firms are reputable operators in the self build sector.

While the exemption for self build is clear, the situation around custom build homes needs further clarification. NaCSBA highlighted this in its response to the consultation, where it concluded that, given the relative scale of the sector and the challenges of separating self-build and custom build, the best approach was to use the current legal definition. This covers both self and custom build and, on this basis, custom build should also be exempt.

NaCSBA will be seeking clarity around this, as it is unclear where the options for some custom build schemes, as each one is slightly different.

The new Homes Ombudsman will be able to hold developers to account and require them to put matters right in the case of a complaint, and it can even prevent developers from trading in the future if they fail to meet the expected standards.

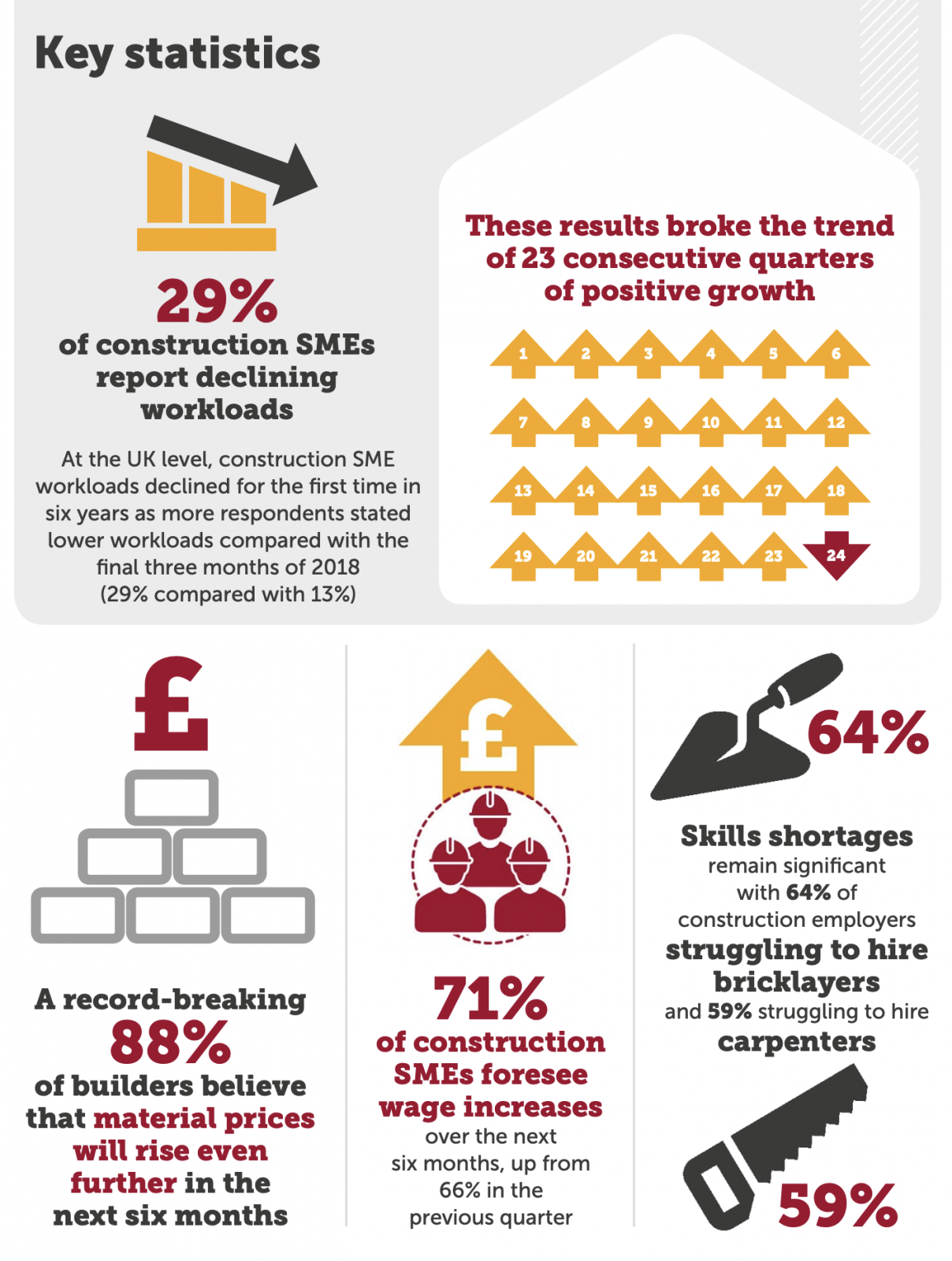

Research by the Federation of Master Builders has pointed to a dip in the workload for small and medium-sized(SME) construction firms for the first time in six years. The FMB’s State of Trade Survey for Q1 2019 has found that SME firms have now moved into negative movement in terms of construction, following a years of uncertainty around Brexit, with materials rising in cost and a skill shortage continuing to take its toll.

Brian Berry, Chief Executive of the FMB, said: “This dip follows three years of political uncertainty, which have taken their toll on the SME construction sector. A perfect storm of diminished consumer confidence, rising material prices and increases in wages and salaries has resulted in the construction SME sector detracting for the first time in six years.

“These results are also very much in line with recent stats from the ONS and PMI data, all of which point to a wobble in the construction industry. Consumers and businesses alike are understandably putting off large investment decisions while the never-ending Brexit negotiations rumble on.

“Worse still, our latest research reveals record-breaking results for expected material price rises with almost 90 per cent of firms predicting that they will increase further in the coming months. This is bad news for builders and consumers alike as construction projects, large and small, become more expensive to deliver.”To support the industry and stimulate growth, the FMB is campaigning for the Government to cut the VAT on home improvement work. This would see a reduction in VAT from 20 per cent to 5 per cent on all housing repair, maintenance and improvement (RM&I) work. The FMB believes that reducing VAT on RM&I work could boost the UK economy by more than £15bn over a five-year period, which is supported by independent research by Experian.

Berry concluded: “The Government must do what it can to boost the economy during this time of political uncertainty and that’s why we’re calling for a reduction in VAT. Such a VAT reduction has the backing of more than 60 charities, trade associations, business groups and financial firms as there is no other policy that would achieve so many of the Government’s economic, environmental and social aims with so little cost to the public purse. At a time of continued political uncertainty and a dip in construction output, a VAT reduction for RM&I is exactly what the UK economy is crying out for.”

The report was compiled by Experian in Q1 2019 from 289 construction SMEs that responded to the survey. The results reflect balances – ie the number of firms reporting a rise in workload against the number of firms showing no change or a fall, giving a qualitative, as opposed to quantitative, overview.